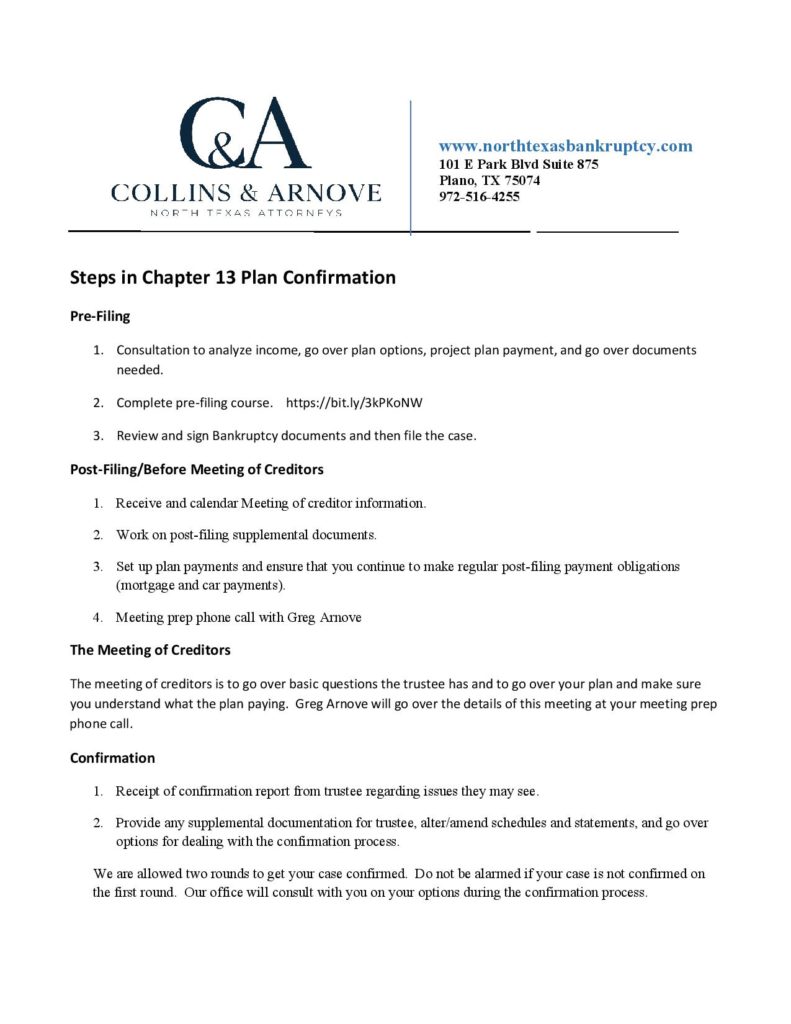

Overview of Chapter 13 Bankruptcy

Chapter 13 is known as a plan of reorganization which in which you must submit a plan to the Court and to creditors that must be confirmed by the Judge. Chapter 13 is useful for people who are behind on certain secured items, behind on the IRS, or who make too much money to file … Read more